According to a survey carried out by the AA a few years back, they found that after mortgage repayments, home maintenance and repairs were the next biggest cost for homeowners. They found that the average home owner will spend (and need to set aside each year) €1,290 every year to keep up with wear and tear in their home.

As with any large, once off, unexpected expense, it can throw our finances out of whack and put a dent in either your savings which were set aside for other purposes or increases the amount of debt we have because we have to borrow to carry out whatever maintenance is required. We know the best way to overcome these shocks are to plan in advance for them and the best way is to build this expense into our monthly budget and set aside a certain amount each month so that when something needs to be repaired, up-graded or replaced you have the money set aside specifically for that purpose. And when people populate the budgeting template for me, the amount they set aside varies from €0 up to the maximum I have seen of €2,000. However, I do think people get confused when recording this amount in their budget because I feel people are putting in an amount they plan on spending on their house for home improvements (non-essential spending) rather than home maintenance (essential spending) Anyway, it is important you don’t confuse the two and what I want you to consider and reflect on is the amount you need to budget for essential repairs. The question of course is how much should you set aside each month? And this is a really difficult question to answer so to help you with this, I did some research as to what the optimum amount should be and I found there were two rules of thumb that I thought made the most sense, were the most practical and were the easiest to remember. And the first rule of thumb is called the one percent rule which states that you should set aside 1% of the value of your home for ongoing maintenance. So, if your house is worth €150,000, you should budget €1,500 each year for maintenance. This figure, or any figure by the way doesn’t mean you are going to spend that amount every year, some years you will spend less and other years you will spend more, but on average and over say 10 years, this is the average amount you will spend each year. The second rule of thumb for the amount you need to budget for home maintenance each year is related to the square footage of your house. For every square foot you should be setting aside €1 for maintenance and repair costs. So, if your house is 1,800 sq ft then you need to be budgeting for an average annual cost of €1,800 over the long term. And this method of determination might make slightly more sense than the first because the more square feet in your house, the more you have to manage and repair as opposed to what the house is valued at. But what you don’t have control over using this rule is the cost of labour and materials which may vary depending on where you live – in certain parts of the country, contractors and the costs of materials could be significantly more expensive. I am going to come back to which rule I personally use at the end of this article, but before I do, I want to look briefly at those factors that make the biggest impact on the amount we spend on our houses each year. And the first is obviously the age of your property. You would like to think that any property built in the last 10 years would need very little maintenance, but the chances are probably good that as a house gets older the cost of maintaining it will increase. My own house is 30 years old and we are in it 12 and we are beginning to see the importance of setting aside money each month because every year we are seeing the amount we are spending on it increase – this year we need to give the heating system a much needed makeover. Another factor that will influence how much you will spend on your house each year is the weather. Friends of ours have a property in West Cork and they tell me that their house is frequently subjected to heavy winds and rain together with long periods of below freezing temperatures and the impact this has on the exterior and interior of their house and the amount they have to spend to repair it each year is significant. There are many other variables that will impact how much you should budget for repairs and maintenance each year, including the location and type of property you have, but that said, I think it is prudent to combine the 1% and square footage rule when figuring out how much you might need each year and this is what I do. If for example your property is worth €250,000 and the square footage is 1,500, then the average of both is €2,000 and that is what you should budget for each year. And furthermore if your property could be adversely affected by its age, weather or location, then add another 10% for each of these factors to the overall amount you should set aside each year. It is hard to predict how much it will cost year on year to maintain your home, and like many other areas of your finances, the best you can do, is make an educated guess and using these rules is a very good starting point.

0 Comments

Single Assessment Under assessment as a single person, each spouse is treated as a single person for tax reasons. With this option:

Separate Assessment Under the separate assessment option, the tax affairs of spouses are independent of each other. The difference between separate assessment and assessment as a single person is that under this option, some tax credits are divided equally between you. These tax credits are:

Joint Assessment The joint assessment (or "aggregation") option is usually the most favorable basis of assessment for a married couple. This option is automatically given by the tax office when you advise them of your marriage but this does not prevent you from choosing to be assessed individually or separately. Under this option, the tax credits and standard rate cut-off point can be allocated between spouses to suit their own circumstances. If only one spouse has taxable income, all tax credits and the standard rate cut-off point will be given to the spouse with the income. If both of you have taxable income, you can decide which of you is to be the assessable spouse. You then ask the tax office to allocate the tax credits and standard rate cut-off point between you in whatever way you wish. If your tax office does not get a request from you to allocate your tax credits in any particular way; the tax office will normally give all the tax credits (other than the other partner's PAYE and expense tax credits) to the spouse being assessed. The spouse being assessed must complete the return of income for the couple and is chargeable to tax on the joint income of the couple. If one spouse is self-employed, joint assessment can still apply. The flexibility this option brings can be very convenient - especially if one of you pays tax under the PAYE system and the other pays tax under the self-assessment system. Under joint assessment, you let your circumstances determine if most of the tax should be paid under PAYE or in a lump sum on assessment. This is determined by the way in which the tax credits are allocated. If you choose to pay most of your tax under PAYE, the tax credits (apart from the PAYE tax credit and employment expenses), should be offset against the self-assessment income. The choice about who becomes the assessable spouse is made by both of you. All you need to do is to inform Revenue which of you is to be the assessable spouse. If you have not made your nomination, the assessable spouse with the higher income in the latest year for which details of both spouses' incomes are known becomes the assessable spouse. This person continues to be the assessable spouse until both of you jointly elect that the other spouse is to be the assessable spouse or until either of you opts for either separate assessment or assessment as a single person. In my opinion it is much more beneficial to be assessed jointly rather than individually so I would suggest that if you are married but taxed individually you should notify the Revenue if you have not done so already and ask them to change your method of assessment to joint. And who knows if you forward them your P21’s for the last few years for both of you (the year of marriage will not be factored into calculations for joint assessment) you may even be due some tax back.

And financial therapy, which is growing in popularity, is exactly what it sounds like, a combination of psychology and financial advice, the problem, however, for people is that financial advisors will only focus on numbers and feel uncomfortable talking about people’s emotions and on the flip side, therapists are not trained in dealing with money but are happy to talk about people’s emotions.

Like any other disorder, a money one is where there is a persistent pattern of self-destructive behaviour and according Brad Klontz, who is a leading expert in this area, they begin at a very early age, where we get distorted beliefs about money, which Klontz refers to as "flash points" - these are painful distressing and dramatic life events associated with money that are so emotionally powerful, they leave an imprint that lasts well into adulthood. And I absolutely get this because I meet so many people every week who have particular issues and struggles with money and when you talk a little bit more with them and dig a bit deeper, it becomes obvious why this is the case because more often than not an incident happened in their past that continues to affect them and their relationship with money. In a survey carried out last year, it was found that people feel more shame around money issues than they do around sexual problems - lying to their spouse about their spending, feeling guilty about how much money they make, spending money to make them feel better (doesn't last long by the way), not spending money at all, are just some of the disorders people suffer from but the top five most commonly recognised money disorders are: 1. Frugality 2. Denial 3. Dependency 4. Rejection 5. Enabling I think we all know someone who we think still has their communion money, but for them the reason they don't spend money is not because they enjoy saving money, the reasons run much deeper. About six months ago for example, I met with a very successful lady in her mid 40's, who had risen through the ranks and was now a senior vice president in a multi-national IT organisation. She had more money than she could spend but that was her problem, she wouldn't spend any money on herself or her family. She was incredibly insecure about money and was always worrying that if she ever lost her job, she would run out of money so she hoarded it. After about an hour of chatting, she shared with me that she was the eldest from a family of seven and was raised above a pub in Kerry where her father was the proprietor. She broke down while telling me how her father had been an alcoholic and any money he made, he drank. Herself, her siblings and her mother often went without food because they had no money and she saw the impact it had on her sisters and her mother, so subconsciously I think she vowed to herself that when she was older, she would never run out of money and one way of doing this is never to spend it and never stop earning it. The difficulty with this type of person is that they are hard to cure because they don't see anything wrong with their behaviour. They live in a constant fear of financial ruin and will always worry that they will end up destitute no matter how much money they have. They put off buying things that would make a positive difference to their life, because they don't want to spend any of their money. And the problem with what we have gone through as a nation in the past eight years is that we may have bred a whole new generation who will suffer from this disorder - that is the children whose lives have changed dramatically because their parents lost their homes or jobs due to the recession. If you think, you, your spouse or someone you know, suffers from this type of disorder, well some help is at hand because research carried out by social scientists show that the following strategies can actually help: 1. Use plastic instead of cash - you would think that someone who hates spending money would never use credit cards but it has been proven that when they do, they will spend more than if they were to use cash so getting them to use a pre-paid credit card would be a good thing 2. Focus on long term benefits - under spenders are more likely to part with their money if they believe the purchase is a good long term investment. Joining a gym for example and getting healthier will improve their health and reduce their future medical expenses. 3. Bundle purchases - under spenders hate buying individual items but they really like buying things that come in a bundle like phone/internet/tv packages and if they decide to go on holiday, guess which one they will go on - yes you are right - the all-inclusive one. In Ireland we all know what we should be doing - spend less and save more - so more information about how we spend our money is not going to help - we need to look deeper at the emotional issues behind the problem - When you think about dieting and exercising for example, most people know that if you exercise more and eat better your health will improve, so why don't we act on this information instead of becoming the second most obese nation in Europe - it appears to me that we cannot blame a lack of information and understanding for these problems and the same goes for money issues - getting to the root of doing things that you really don't want to be doing whether that is over or underspending, lying to your partner about debt or feeling guilty about how much you earn are emotional problems that we need to help people with. Next week I will look at the other money disorders people suffer from, identifying their symptoms and looking at what coping mechanisms and strategies they can take to help manage them better.

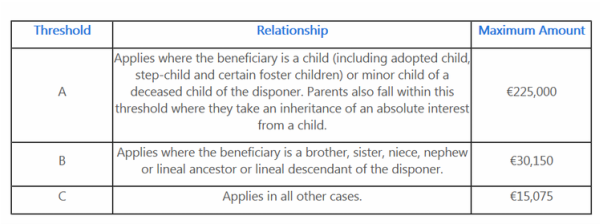

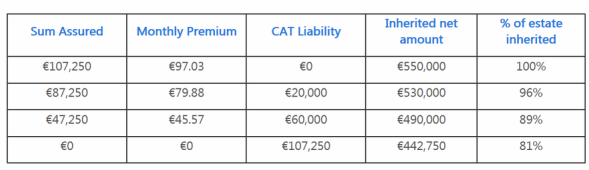

The amount you can gift or inherit from someone depends on your relationship with them. There are currently three bands that have different thresholds at which they can receive a lump sum without incurring any liability and they are:  Anything above each threshold is taxed at 33% - so the value of what a child would inherit would have to be not greater than €225,000 before capital acquisition tax (CAT) kicks in. If someone for example was to inherit a property worth €450,000 and cash worth €100,000 then the amount that would be payable to Revenue would be €107,250 i.e. €550,000 - €225,000 x 33%. The threshold amounts have gradually come down each year whilst the tax rate has increased. For example back in 2009, a child could inherit €542,544 from a parent, and the balance was taxed at 22%. Anyway, is there anything that can be done to prevent this from happening? And the answer is YES. There is a life assurance policy often referred to as a Section 235a policy which is arranged for the specific purpose of providing funds on death to pay inheritance tax likely to arise from the death of the policy holder. The term Section 235a refers to the section of the Capital Acquisitions Tax Consolidation Act 2004 which provides a relief for inheritance tax for the proceeds of policies arranged for this purpose. The proceeds of a Section 235a policy are also exempt up to the amount of any approved retirement fund (ARF) tax arising from the death of the deceased policyholder. If we look at the figures I have just used, the cost of putting a policy in place to eliminate an inheritance liability of €107,250 for a 45 year old male would be €97.03 per month (this monthly premium is the best in the market and is with Irish Life) Let me give you an example of what this would look like and what other amounts would cost as well:  I think it is worth looking at this further based on the value of your own estate and what your children will be faced with now when you are young enough to do so because as you get older and your estate becomes more valuable, the cost of taking out such a policy would be so large it would really become prohibitively expensive.

I have come across many people who are inheriting money from their parent’s estate and the amount they have to give away in inheritance tax is enormous and they only wish their parents knew of or took out such a policy when they were young enough to do it. It would have saved them hundreds of thousands of Euros, and of course some parents take the view that the amount their children inherit is going to be large anyway even after paying Revenue so it depends on your outlook. There is a second way of avoiding incurring this liability particularly if the property you inherit is your principal place of residence along with other conditions that are

|

Archives

September 2015

Liam CrokeManaging Director of Harmonics Financial Categories |

Harmonics Financial Ltd., Registered Office Mary Rosse Centre, Holland Road, National Technology Park, Limerick. Directors: Liam Croke QFA BBA LIAM, John Fitzgerald

Incorporated in the Republic of Ireland, Central Bank of Ireland No: C86227. CRO No: 481477

Harmonics Financial Ltd. is regulated by the Central Bank of Ireland.

Incorporated in the Republic of Ireland, Central Bank of Ireland No: C86227. CRO No: 481477

Harmonics Financial Ltd. is regulated by the Central Bank of Ireland.